Did OpenAI and Anthropic's $11.5Bn PE Pact Just Decide Indian IT's Future?

- AltG Investment Research Lab

- May 9

- 3 min read

The NIFTY IT correction priced in fears of AI disruption. May 4 made the math binding — and the structural moat just got a name.

The NIFTY IT index has already fallen ~17% YTD in 2026, hit a 30-month low in February, and underperformed the broader NIFTY 50 by roughly 15 points. The sell-off was driven by what investors called "AI fears" — vague, sentiment-based, with brokers like CLSA finding no actual evidence of pricing pressure in deal renewals.

May 4 made those fears concrete.

On May 4, OpenAI and Anthropic each announced joint ventures with the largest names in private equity:

OpenAI's "Deployment Company" — a $10B vehicle backed by TPG, Brookfield, Bain Capital and Advent. Already in advanced talks to acquire three AI services firms outright.

Anthropic's JV — a $1.5B vehicle backed by Blackstone, Hellman & Friedman, Goldman Sachs, Apollo, General Atlantic and Sequoia. Mandate: embed engineers inside mid-market companies and rebuild workflows around Claude.

Combined: ~$11.5B committed in 24 hours, structured to deploy AI directly inside operating companies — not to sell more software licenses. The full deal structure is in Who Owns Intelligence?.

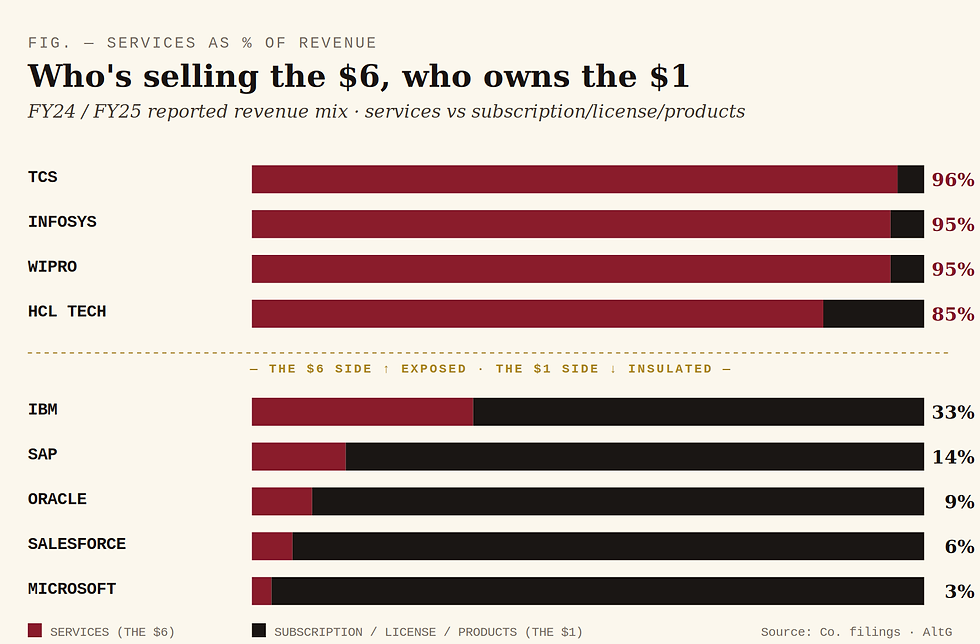

What makes the move aggressive is what they are aiming at. For every $1 an enterprise spends on software (the license, the subscription), it spends roughly $6 on services to make that software actually work — implementation, integration, customization, change management, training, ongoing operations. That $6 is a >$2 trillion pool globally, and it has historically belonged to the consulting industry — McKinsey, Accenture, Deloitte, IBM Consulting — and to offshore IT services.

The labs' play is to use forward-deployed engineers and AI agents to re-margin the $6 from ~15% net today to 35–50%, by collapsing the labor cost structure underneath it.

That $6 bucket is where Indian IT lives. ADM, systems integration, managed services, BPO, transformation consulting — TCS, Infosys, Wipro and HCL run 85–96% of revenue out of these exact line items.

The chart maps the divide. Indian IT and the consultancies sit on the high side, far above 80%. The big software companies — Microsoft (3%), Salesforce (6%), Oracle (9%), SAP (14%) — sit on the low side. IBM is the only meaningful hybrid at 33% — and that exposure is exactly why IBM is restructuring Consulting around AI as we speak.

The companies that own the $1 are insulated. The companies that sell the $6 are exposed. Indian IT has spent two decades selling labor at scale and built almost no $1.

The disruption is not immediate. Multi-year contracts and embedded delivery processes give the Tier 1s 2–3 years of lead time. Citrini Research and JP Morgan have already flagged contract cancellation risk accelerating through 2027.

The question for the NIFTY IT is no longer whether AI disrupts the sector. It is what these companies have built besides offshore delivery.

The market correction was directionally right. May 4 just made the math binding.

Disclaimer: This editorial is for informational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. All forward-looking statements, scenarios, and market share projections are illustrative editorial estimates based on publicly available information and are subject to change. Stock prices are highly volatile; past performance is not indicative of future results. Readers should conduct their own research and consult a qualified financial advisor before making any investment decisions. The data cited is sourced from public filings, exchange data, news media and industry research; while care has been taken, errors may exist. Holdings disclosure: not applicable to editorial.

Comments